- HOME

- Procurement

- Purchase orders explained: Why spend control must begin before the invoice

Purchase orders explained: Why spend control must begin before the invoice

If purchase orders feel bureaucratic in your organization, it's rarely because the concept is flawed. It's because they were introduced after decisions were already made, without clarity on who owns the commitment.

Most procurement teams recognize this pattern: a vendor is agreed over email, the work begins immediately, and weeks later an invoice arrives completely accurate, legitimate, and already treated as inevitable. At that point, the organization is no longer deciding, it is confirming.

A purchase order exists precisely at the moment intent becomes obligation.

What is a purchase order?

A purchase order (PO) is a formal authorization issued to a supplier before money is committed. Once accepted by a supplier, it clearly confirms:

What is being purchased

- At what price

- Under which commercial terms

- Against whose budget

Purchase requisition vs. purchase order

This distinction is often misunderstood and is operationally critical.

| Purchase requisition = Internal authorization | Purchase order = external commitment |

| An internal request to make a purchase. It secures budget approval and internal authorization but creates no external commitment. | An internal request to make a purchase. It secures budget approval and internal authorization but creates no external commitment. |

Think of this as a two-gate approval system:

Gate 1 - Should we make this purchase? (requisition)

Gate 2 - What exactly are we committing to? (purchase order)

High-performing procurement teams enforce both gates, not just one.

Importance of purchase orders in the procure-to-pay process

Within the procure-to-pay lifecycle, purchase orders sit at the intersection of planning and execution. They translate internal intent, a validated need, an approved budget, and authorized authority into an external commitment a supplier can act on.

When issued correctly, they:

- Fix supplier expectations before work begins

- Assign budget ownership to the commitment

- Lock commercial terms before costs accrue

As a result, invoice verification and accrual accuracy become natural outcomes of the process, not manual checks performed later.

Why purchase orders are critical for spend control

From a finance perspective, purchase orders solve four persistent problems:

| Control areas | Without POs | With POs |

| Budget visibility | Spend becomes visible only when invoices arrive. | Commitments are visible at approval. |

| Spend ownership | Authorization is unclear and through informal channels. | Requester, approver, and cost center are documented. |

| Invoice verification | AP manually validates every invoice. | Invoice matches against approved price and quantity. |

| Audit defensibility | Approvals are reconstructed after the invoice. | Policy-compliant approval is recorded before obligation. |

Common objections to purchase orders

"Purchase orders slow teams down."

Poorly designed approvals slow teams down. Purchase orders simply surface decision points that already exist.

"We only need POs for large purchases."

Small, unplanned purchases compound into material variance. The question is not size; it is risk, frequency, and repeatability.

"Invoices are enough."

Invoices confirm charges. They do not confirm authorization.

Types of purchase orders

Different purchasing patterns require different PO structures. Choosing the right type is not about formatting, it's about encoding the right control decision once, so teams don't guess every time.

These templates are designed around purchasing behavior, not layout preferences. Each one standardizes a different approval and commitment question.

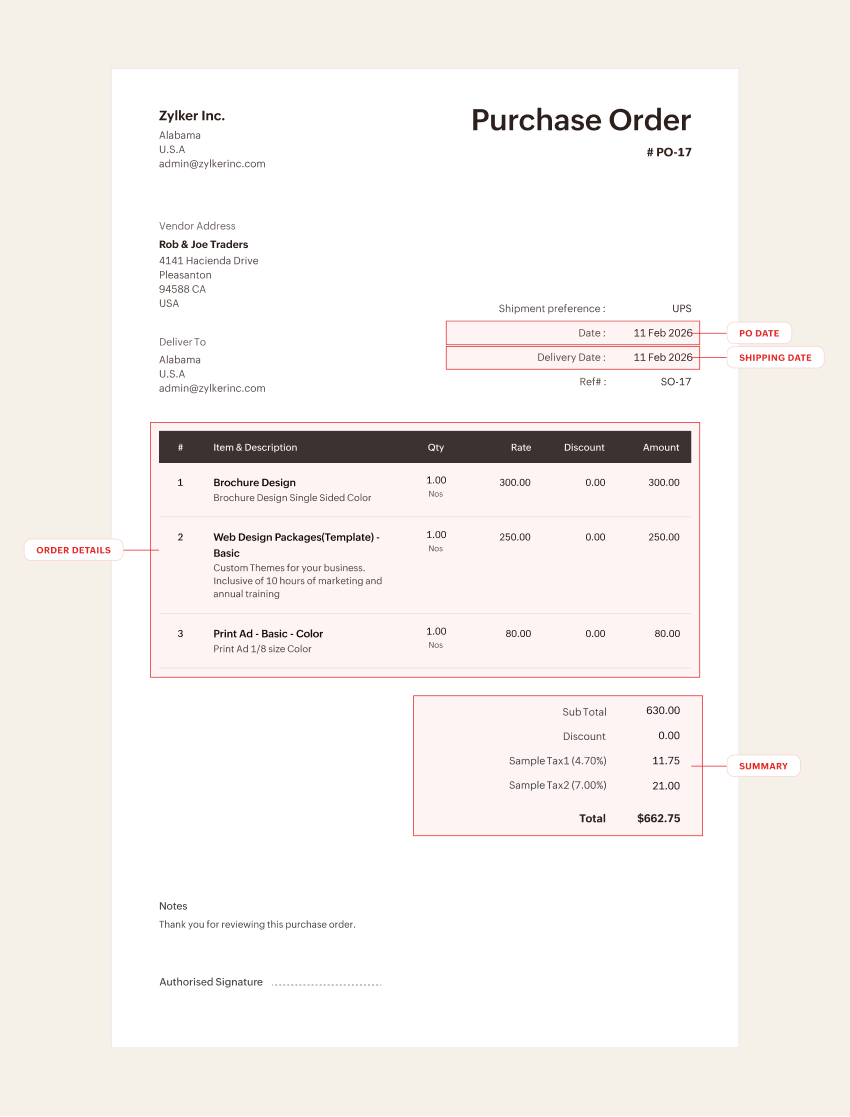

Standard purchase orders

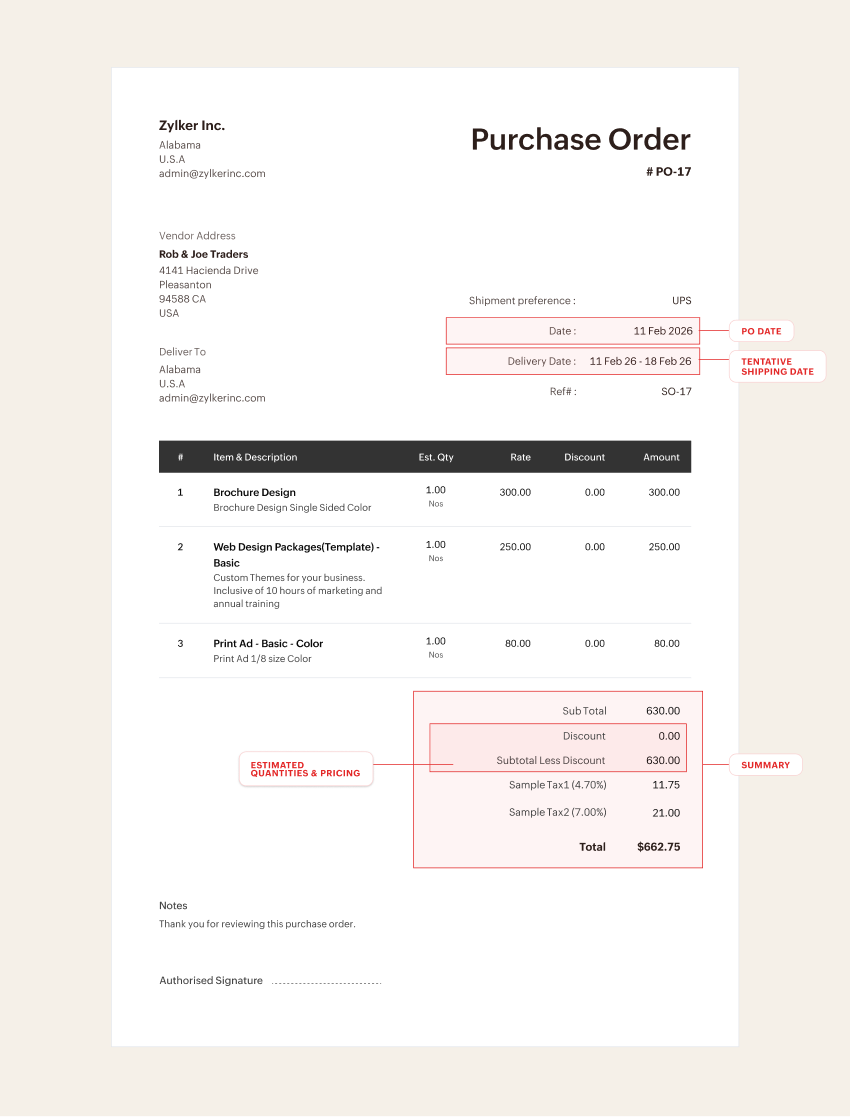

Planned purchase orders

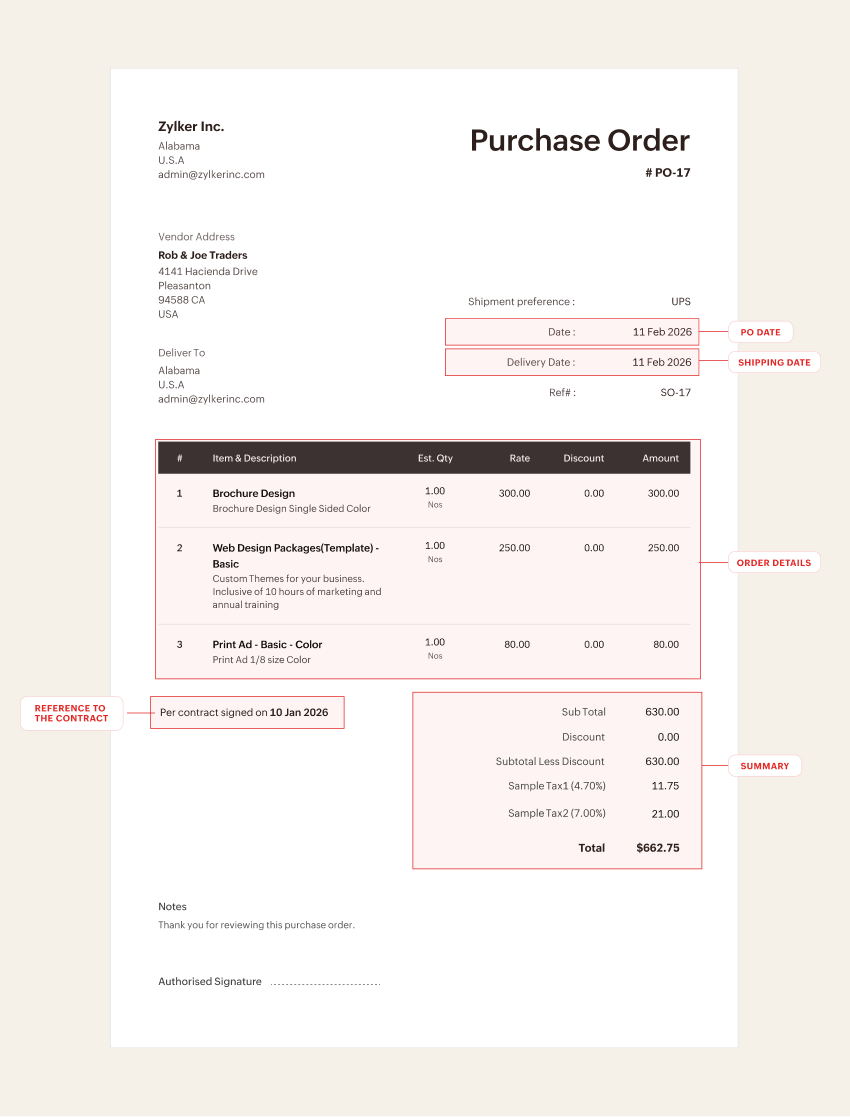

Contract-linkedin purchase orders

Blanket purchase orders

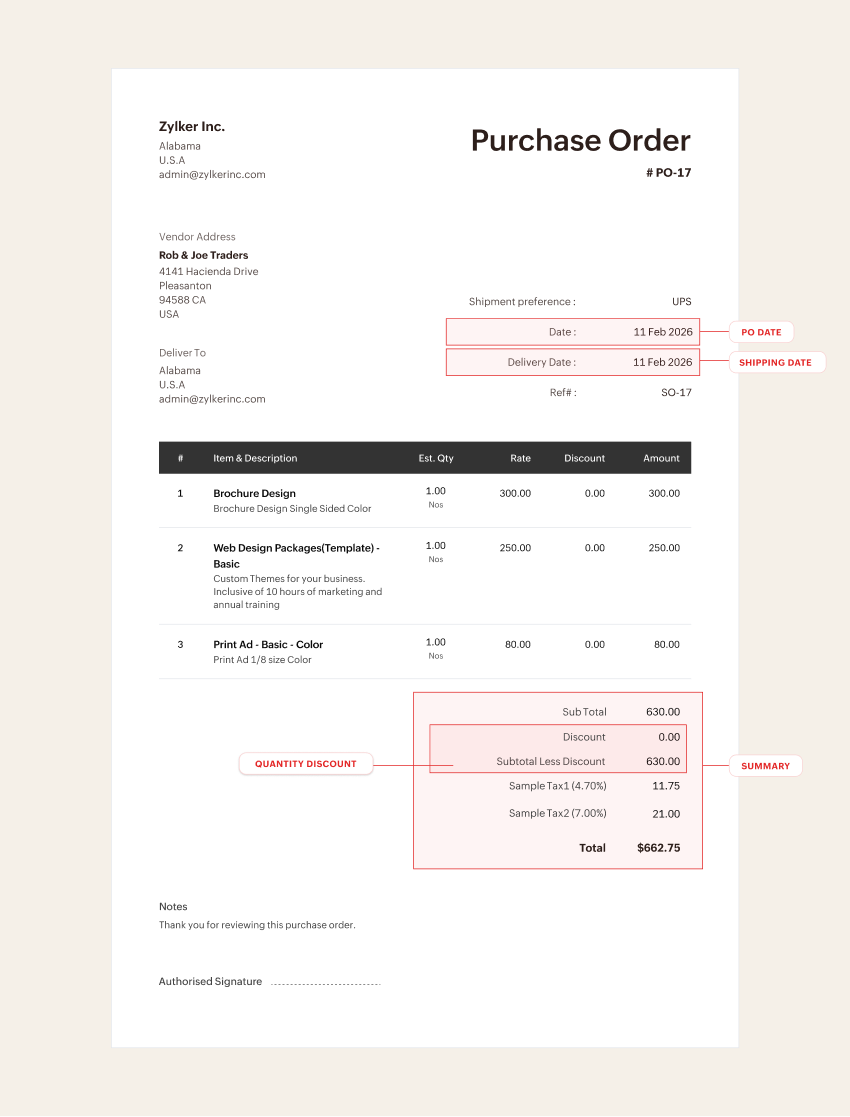

What a purchase order must include

A purchase order should remove ambiguity at the point of commitment.

At minimum, it must clearly define:

- Unique PO number for traceability

- Buyer and supplier legal entities

- Precise item or service descriptions

- Quantities, unit pricing, and totals

- Delivery or service timelines

- Payment terms and tax treatment

- Contract or catalog references

Precision here prevents disputes, rework, and invoice mismatches later.

Measuring purchase order effectiveness

High performing teams don't measure success by PO volume, they measure outcomes.

Common indicators include:

- PO coverage ratio (spend backed by approved POs)

- Invoice mismatch rate

- Percentage of non-PO or unplanned spend

- Cycle time from requisition to PO

- PO compliance by category or department

These metrics help reveal whether purchase orders are enabling control or merely existing.

Closing perspective

Purchase orders are often treated as paperwork because they appear at the end of the process. But their value comes from being used at the beginning, when a decision becomes a financial commitment.

They don’t exist to slow purchasing. They exist to make responsibility explicit, budgets predictable, and verification effortless later.

Organizations that rely on invoices to create control are correcting decisions after money moves. Organizations that rely on purchase orders are shaping decisions before money moves.

The difference is not administrative, it is operational discipline.